Navigating healthcare coverage decisions can be complex, especially when you're eligible for Medicare while still having access to employer insurance. Many working Americans approaching or over 65 face important choices about combining Medicare with their existing employer coverage. Understanding how these two types of insurance can work together is crucial for making informed healthcare decisions.

This comprehensive guide will help you understand the relationship between Medicare and employer insurance, including when you need to enroll, which insurance pays first, and how your choices might affect your healthcare coverage and costs.

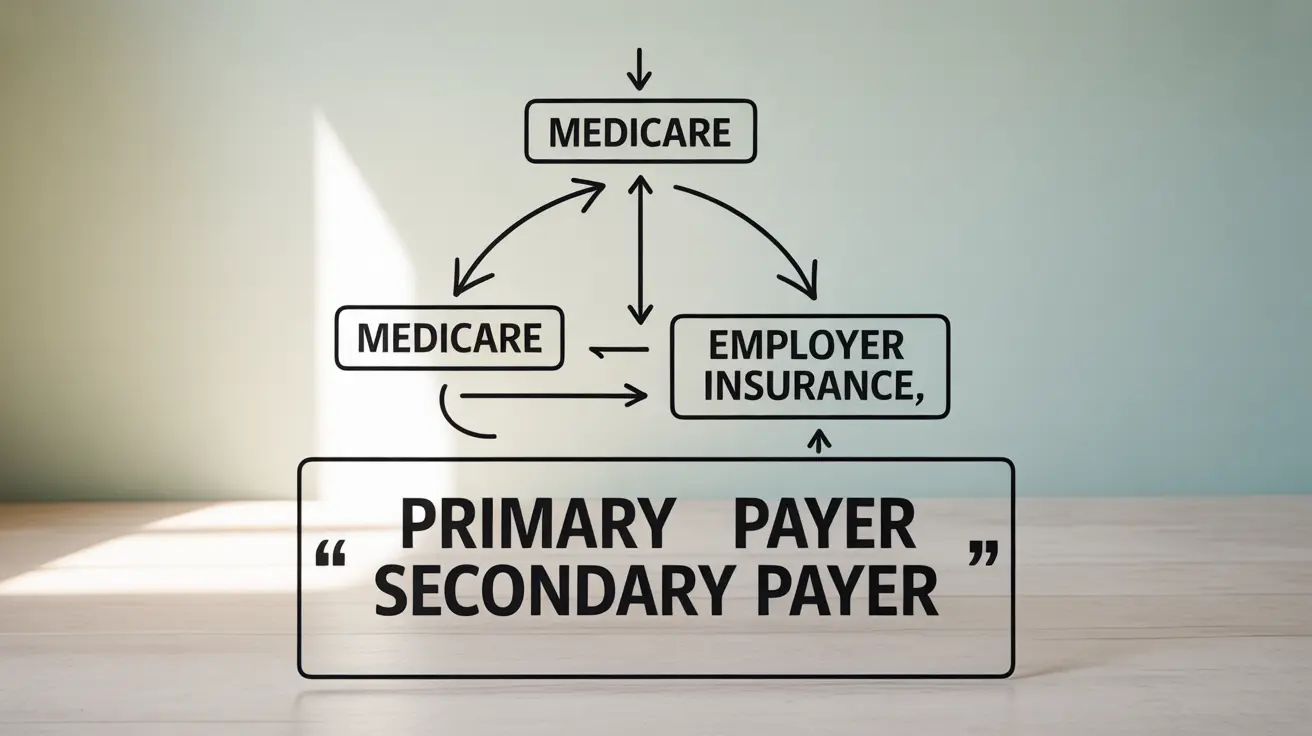

How Medicare and Employer Insurance Work Together

Yes, you can have both Medicare and employer insurance simultaneously. However, several factors determine how these coverage types coordinate and which one serves as your primary insurance. The most important factor is your employer's size, as this affects both your enrollment requirements and how claims are processed.

Large Employer Coverage (20+ Employees)

If you work for a company with 20 or more employees, your employer group health plan will typically be your primary insurance, with Medicare serving as secondary coverage. In this situation, you have the option to delay enrolling in Medicare Part B without penalty, as long as you maintain your employer coverage.

Small Employer Coverage (Less than 20 Employees)

For those working at smaller companies with fewer than 20 employees, Medicare generally becomes the primary payer, with employer insurance serving as secondary coverage. In these cases, it's usually advisable to enroll in Medicare Part B when first eligible to avoid gaps in coverage.

Coordination of Benefits: Understanding Who Pays First

The coordination of benefits between Medicare and employer insurance follows specific rules established by federal law. These rules determine which insurance pays first (primary payer) and which pays second (secondary payer).

Primary insurance always processes claims first, paying up to the limits of its coverage. The secondary insurance then considers the remaining costs, potentially covering some or all of the remaining balance according to its policies.

Impact on Health Savings Accounts (HSA)

An important consideration when combining Medicare and employer coverage is how it affects Health Savings Account contributions. Once you enroll in any part of Medicare, including Part A, you can no longer contribute to an HSA. However, you can continue using existing HSA funds for qualified medical expenses.

HSA Contribution Rules

If you plan to continue contributing to an HSA, you may want to delay Medicare enrollment if you're still covered by a qualifying high-deductible health plan through your employer. However, be sure to understand the implications and timing of your Medicare enrollment to avoid penalties.

Making Informed Enrollment Decisions

When deciding whether to enroll in Medicare while having employer coverage, consider these key factors:

- Cost comparison between your employer plan and Medicare

- Coverage needs and whether having both types of insurance provides additional benefits

- Your employer's size and how it affects primary/secondary coverage

- Whether you contribute to an HSA and want to continue doing so

- Your planned retirement date and future healthcare needs

Frequently Asked Questions

Can I have both Medicare and my employer's health insurance coverage at the same time?

Yes, you can have both Medicare and employer insurance simultaneously. How they work together depends primarily on your employer's size and whether you're actively employed or retired.

How do I know which insurance pays first if I have both Medicare and employer coverage?

For employers with 20 or more employees, the employer insurance pays first. For smaller employers (fewer than 20 employees), Medicare typically pays first. This is determined by the Medicare Secondary Payer rules.

Should I enroll in Medicare Part B if my employer has fewer than 20 employees?

Yes, it's generally recommended to enroll in Medicare Part B if your employer has fewer than 20 employees, as Medicare will be your primary insurance. Not enrolling could leave gaps in your coverage.

What happens to my Medicare enrollment if I work for a large employer with 20 or more employees?

If you work for a large employer, you can delay enrolling in Medicare Part B without penalty while maintaining your employer coverage. You'll qualify for a Special Enrollment Period when you eventually leave your employer coverage.

How does having Medicare affect my ability to contribute to a Health Savings Account (HSA) while working?

Once you enroll in any part of Medicare (including Part A), you can no longer contribute to an HSA. However, you can continue using existing HSA funds for qualified medical expenses.